Direct bank payment transactions

In the UK we have embraced non-cash payments more than just about any other country.

The main argument against (along with big brother and ‘reliant on the system’ concerns) is the cost for small businesses.

This is sometimes over stated, fees tend to be 1-2% max and handsets are very cheap (and your phone can act as one). For example Stripe is 1.5% +20p, and SumUp (click ‘see all fees’) 0.99% for in person, more (1.69%) for AMEX, and 2.5% for online, plus £19/Month. When you factor in cash has banking costs, risks and time, this doesn’t see too bad.

A recent factor is the US card networks (Visa, Mastercard, Amex) bending to US political pressure. We live in a world of double speak, especial when it comes to Freedom where those who shout it the most seem to the most blatant restrictors. Whole industries can be cut off from taking payments. Perhaps most shocking is the Judge who sat of the International Criminal Court, the US disagreeing with her judgment has led to her locked out from all bank cards as well as major US firms like Google and Amazon.

There are various efforts around the world to develop home grown payment systems and remove dependencies on these firms. The UK already has something in place ‘pay by bank’.

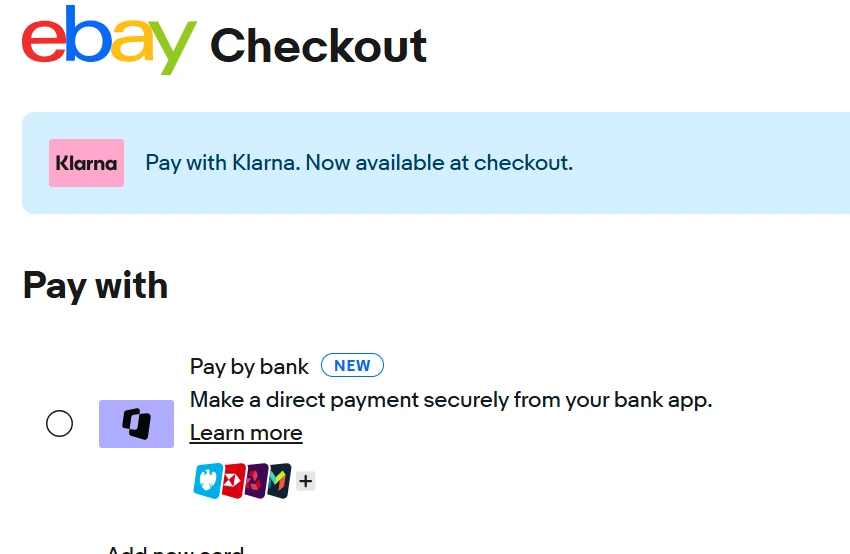

What’s prompted me to write this is it’s come up as an option to pay online a couple of times now and it’s good to see it is picking up. The first was when I made a very rare payment on ebay, the second was when I needed to make a payment on gov.uk.

The Openbanking API performance webpage has a ‘sucessful payments’ chart which documents growth over time.

It’s not totally new, it uses the same basically technology that allows anyone to pay anyone else with a bank account number and sort code (faster payments). Sitting on top of this is a UX which replaces the need to enter any banking details. For example for both my examples I was using a laptop, having selected ‘pay by bank’ and then selected my bank, it provides a QR code to scan with your phone’s camera. This opens your banking app with all the details on screen, selecting ‘approve’ completes the transaction and the webpage on your laptop is updated.

Because the transaction is from bank to bank, there are no other middlemen to take a cut, which should mean lower costs for merchants. The downside is the consumer protection built in to credit and (to a lesser extent) debit cards isn’t yet part of this, as Martin Lewes warns.

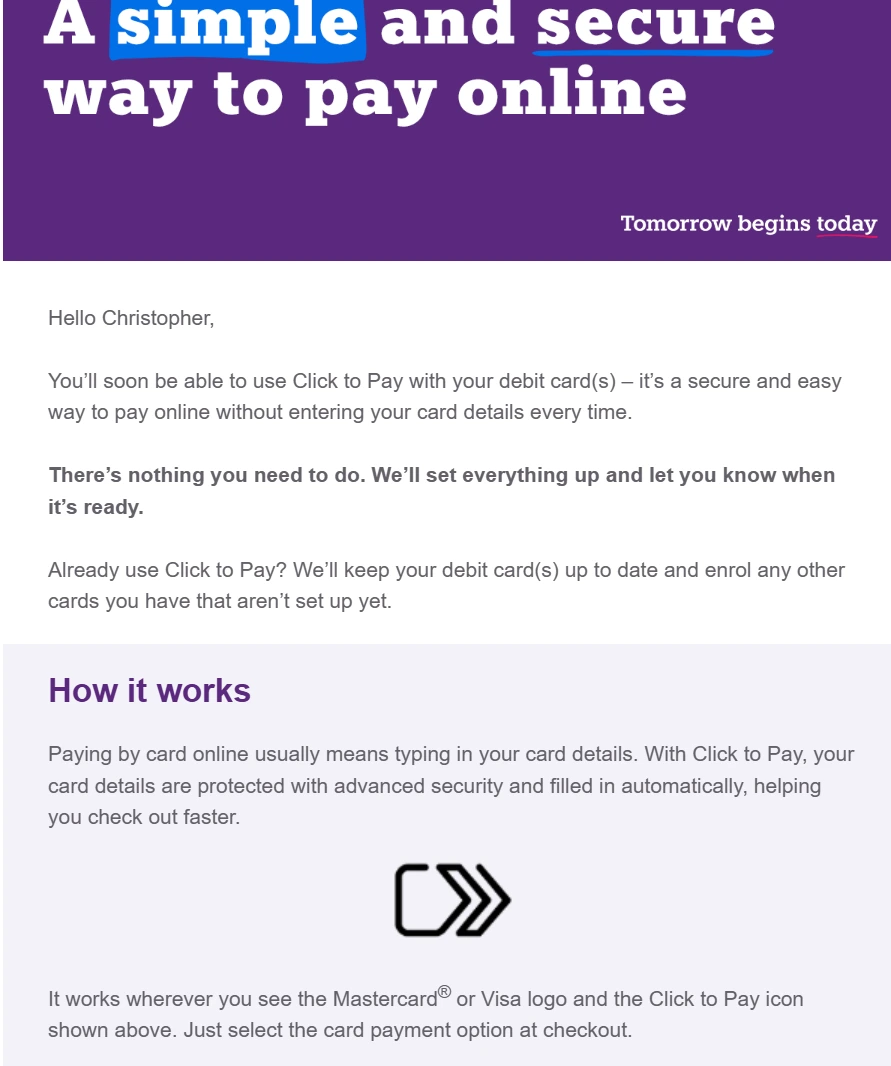

Another thing what prompted to write this was by main bank emailing me about it. Another sign of take up. Only it wasn’t. It was for something else, called ‘Click to Pay’. This works in a very similar way for the end user, no details to enter, but under-the-hood is still mastercard and visa. My guess is that as this still generates nice card fees for consumer banks they are keen to promote.

For me, the independence and more efficient (less players needing a cut) design make ‘pay by bank’ much more desirable.

Finally, this shouldn’t be confused with longer term work to improve the payments infrastructure which supports all this.